A recurring comparison haunts the Korean robotics sector: a domestic component costs KRW 100,000, while a Chinese alternative costs KRW 3,000. While many blame labor costs or lack of scale, the truth is more profound. This isn’t a cost gap—it is a structural architecture gap between two different manufacturing philosophies.

1. Systems vs. Components: The Strategic Divergence

Korea and China built their industrial ecosystems on opposite foundations:

- China (Component-Centric): Built from the bottom up. By focusing on actuators, reducers, and sensors as standalone industrial units, China can flood the market with cheap parts that “work well enough.”

- Korea (System-Centric): Built from the top down. Korea optimized for process design and line integration. We excel at making a factory line run perfectly for a decade, but we struggle to produce the individual “bricks” (components) that build those lines.

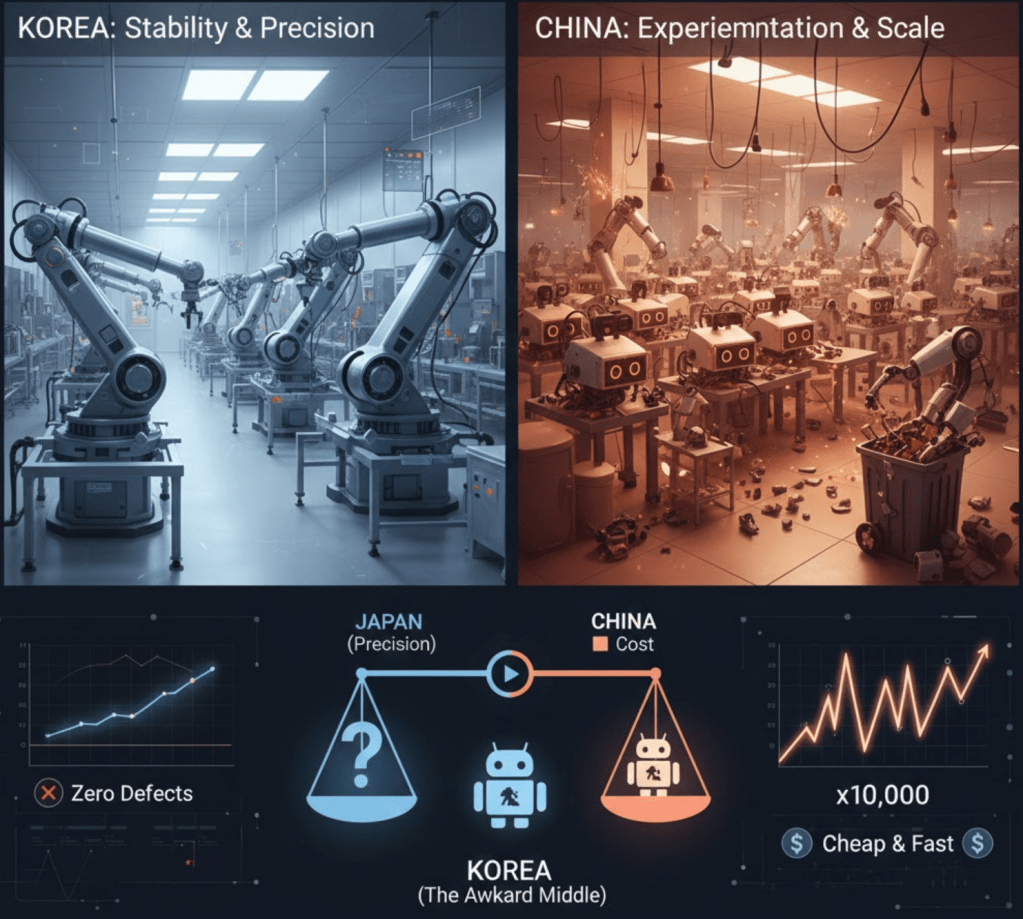

When looking at a robot, Korea sees a finished system; China sees a collection of components.

2. Squeezed in the Middle: Japan vs. China

The data as of 2026 remains sobering. Korea’s localization rate for core functional parts is still stuck in the 40% range.

- Japan (The “Must-Not-Fail” Zone): Japan owns high-precision servos and harmonic reducers where failure is unacceptable. When precision is the priority, buyers pay the premium for Japan.

- China (The “Can-Fail-and-Replace” Zone): China owns sensors and basic actuators where failure is tolerable. When price is the priority, China wins decisively.

Korea sits in the uncomfortable middle: not as precise as Japan, not as cheap as China.

3. The Physical AI Shift: Trial-and-Error over Stability The rise of “Physical AI” is further tilting the scales. Unlike traditional fixed automation, Physical AI requires rapid iteration and massive amounts of trial-and-error data.

- China’s Advantage: They thrive on “disposable” robotics—cheap, experimental units that can fail often during the learning process.

- Korea’s Hurdle: Our manufacturing culture is built on stability and “zero-defect” yields. This makes us slow to iterate on the cheap, experimental hardware that Physical AI demands.

4. The Localization Deadlock

“Localization” in Korea is trapped in a classic chicken-and-egg cycle.

- Low Demand: Because domestic components lack a price edge, robot OEMs continue to import Japanese or Chinese parts.

- No Investment: Without steady demand, component makers cannot invest in the mass-production lines needed to lower costs.

- Import Dependency: As of 2025, Korea still relies on China for nearly 89% of permanent magnets—the very “heart” of robot motors.

5. The Narrow Path Forward: Defensible Precision

For Korea, competing on volume or price against China is a losing battle. The only viable path is the “Precision Moat”—focusing on sectors where failure is catastrophic (defense, medical, or specific humanoid joints). This is a smaller market, but it is one where reliability outweighs the KRW 3,000 price tag.

Final Thought: Cost is the Symptom, Not the Cause

Robot localization in Korea isn’t failing because of a lack of engineering talent. It is failing because our industrial architecture was never designed to produce “parts.”

Until we shift from being a nation of system integrators to a nation of component innovators, the gap between KRW 100,000 and KRW 3,000 will remain a structural reality. In the era of Physical AI, the winner isn’t the one who builds the best factory, but the one who owns the components that learn.

댓글 남기기