Satellites are no longer just part of the space industry.

They are becoming one of the most strategic layers of national power. That is why the market is starting to treat space less like a distant technology theme and more like a core infrastructure sector tied to defense, communications, intelligence, and sovereignty. The money is following that shift. U.S. defense-linked space spending has grown so large that it now sits above NASA’s fiscal 2025 budget level, while private investment continues to flow into launch, low-Earth-orbit networks, and dual-use satellite systems.

1. Why satellites matter right now

The simple answer is national security.

Space has become a core military and strategic domain, not a prestige project. That is why government budgets are rising, and why commercial satellite systems are now being treated as critical infrastructure. Reuters reported in January 2026 that global investment in space technology was expected to rise further, driven heavily by defense-linked satellite systems and launch capacity. At the same time, NASA’s fiscal 2025 budget level was about $24.8 billion, which gives useful context for how large the broader U.S. national space effort has become.

The deeper point is this:

space is no longer optional infrastructure.

It is becoming part of the hard architecture of power.

2. The low-Earth-orbit era is beginning in earnest

The center of gravity in satellites is moving toward LEO, or low Earth orbit.

Why? Because LEO offers lower latency, lower launch cost per mission profile, and stronger usefulness for both communications and Earth observation. That is why the biggest constellation projects in the world are concentrated there. ESA’s space-economy report and Payload’s constellation tracking both show that the next generation of global satellite infrastructure is increasingly LEO-based, with projects measured not in dozens of satellites, but in thousands and in some cases tens of thousands of planned units.

That matters because once LEO becomes the main operating layer, the industry stops looking like bespoke aerospace manufacturing and starts looking more like industrial-scale infrastructure buildout.

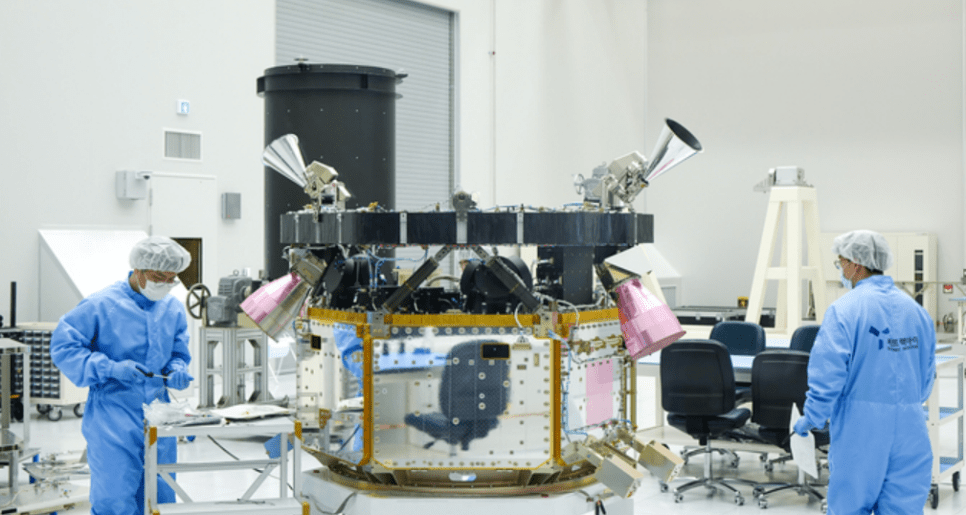

3. The satellite industry is turning into a manufacturing industry

This is one of the biggest changes.

Low-Earth-orbit small satellites typically have shorter useful lives than traditional large geostationary systems, which means replacement demand becomes structural. Once constellations grow, repeat production matters just as much as the initial launch. That is why satellite manufacturing is starting to resemble a volume business rather than a one-off engineering project. Hanwha’s Jeju Space Center is a good example of how this shift is already being taken seriously in Korea. Multiple reports say the facility is designed to produce up to eight satellites per month and about 100 per year, making it the country’s largest private satellite mass-production base.

In other words, the satellite industry is moving from demonstration to repetition.

And repetition is what turns a theme into a real industry.

4. Reconnaissance satellites are becoming a core military layer

One of the clearest areas of demand is surveillance and reconnaissance.

South Korea’s 425 Project is the clearest example. The project consists of five military reconnaissance satellites in total: one EO/IR satellite and four SAR satellites. Reuters and other reporting have tracked the step-by-step deployment of this constellation, and by late 2025 the fourth SAR satellite had already been launched successfully.

That matters because it shows how military space demand is evolving.

This is not about one symbolic satellite anymore. It is about building an operational constellation that improves revisit rate, resilience, and independent intelligence capability.

5. The real logic of Earth observation is SAR plus EO

The most important observation architecture is not either-or.

It is SAR plus EO together.

SAR satellites are valuable because they can observe targets regardless of clouds, darkness, or weather. EO satellites are valuable because they deliver sharper visual identification. In practical terms, SAR is often better for finding and tracking, while EO is better for identifying and confirming. South Korea’s 425 Project reflects exactly that logic through its 4 SAR + 1 EO/IR structure.

That is why the future of reconnaissance is not just higher resolution.

It is sensor fusion.

6. Hanwha is building more than a parts business

Hanwha’s position is interesting because it is not just supplying components.

The group is building an ecosystem. Hanwha Aerospace is tied to launch and broader aerospace systems, Hanwha Systems is focused on SAR satellites, ground systems, and defense-electronics integration, and Satrec Initiative gives the group an EO and imagery-services layer. That makes the Hanwha stack look less like a fragmented supplier network and more like an attempt to build a full Korean space-industrial platform.

That is strategically important.

Because in space, the real value does not always sit in one satellite. It often sits in the ability to connect launch, payload, ground systems, and data exploitation.

7. The most important thing about Hanwha Systems is production capacity

Hanwha Systems’ Jeju Space Center is important because it introduces scale.

Recent reporting says the facility can ramp up to eight satellites per month and around 100 annually, with mass production of SAR-equipped Earth-observation satellites starting this year. That is a major shift for Korea because it moves the conversation away from one-off satellite projects and toward industrial manufacturing capacity.

In the satellite industry, that kind of capacity matters.

Because whoever can produce reliably at scale gains leverage not only in defense, but also in commercial constellations.

8. The hidden value in Satrec Initiative is data, not just hardware

Satrec Initiative matters for a different reason.

Its value is not only in building satellites. It is in selling what satellites produce. The company presents itself as a GEOINT solutions provider spanning satellite systems, Earth-observation data services, and AI-based geospatial analytics. Its SpaceEye-T platform is centered on 0.25-meter-class very-high-resolution optical imagery, and company updates say the satellite has already completed its first year in orbit.

That is the deeper point.

In the long run, the real margin may sit less in launching the asset and more in owning the imagery, analytics, and intelligence layer built on top of it.

9. Intellian is one of the clearer non-Starlink ground-segment plays

The satellite communications stack needs more than satellites.

It also needs gateways and user terminals. That is why Intellian matters. The company has become one of the key terminal suppliers for the Eutelsat OneWeb network, with products spanning enterprise, maritime, land mobility, and government applications. Its flat-panel and parabolic terminals are already positioned across commercial maritime and enterprise markets, and in 2026 it introduced the OW7MP manpack, a military-grade portable LEO terminal designed for defense and government users.

That is why Intellian can be read as a non-Starlink ground infrastructure beneficiary.

And that matters because the gateway and terminal layer often has to be deployed before the full commercial satellite service scales.

10. The real endgame is not space. It is control

The satellite industry is becoming the next battlefield because it sits at the intersection of three things:

communications, intelligence, and sovereignty.

Low-latency communications, persistent observation, military resilience, and data-driven decision-making all now depend on orbital infrastructure. That is why governments are spending more, private capital is following, and national champions are trying to secure full ecosystems rather than isolated products. Reuters summarized the trend well in January: space infrastructure is increasingly being viewed as a strategic national priority, with countries competing to secure geopolitical advantage through investment.

So the final point is simple.

The satellite race is not really about satellites alone.

It is about who controls the infrastructure above the Earth that shapes power on the Earth.

댓글 남기기