For decades, the solar industry has been chasing a ghost: the Shockley-Queisser limit. This physical ceiling dictates that a single-junction silicon cell can never exceed ~29.4% efficiency.

Today, in 2026, we are finally breaking through. Tandem Solar Cells—which stack a perovskite layer on top of a traditional silicon base—are move from a “promising lab experiment” to a “structural market reset.”

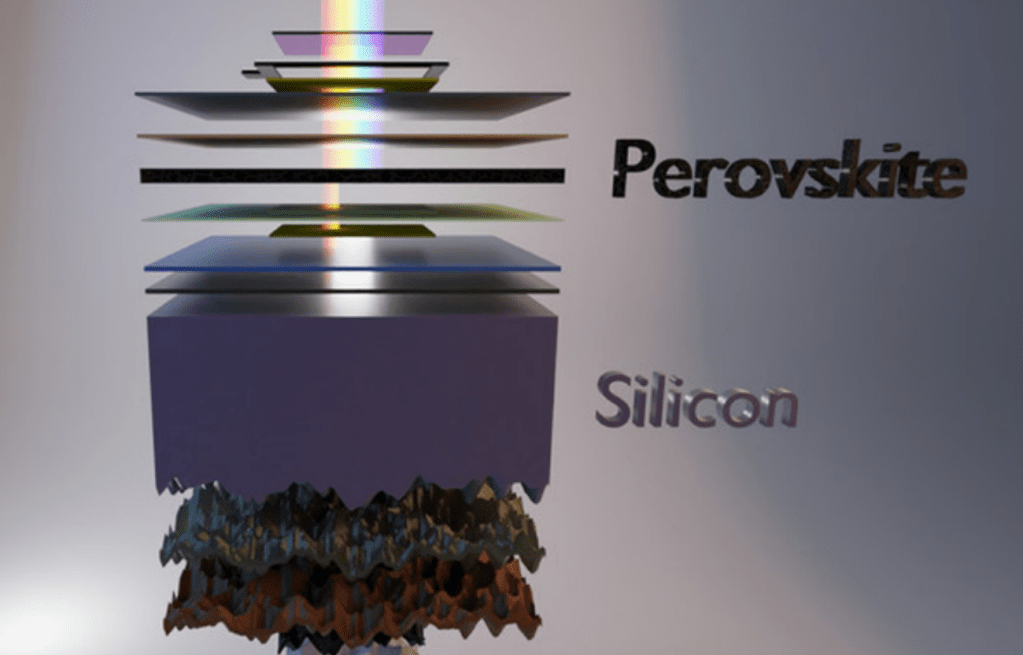

1. Why Tandem? The End of the Silicon Plateau

Standard silicon panels (PERC, TOPCon) have been the workhorses of the energy transition, but they are hitting a plateau.

- The Problem: Silicon is bad at absorbing high-energy blue light (it turns into heat, not power).

- The Commercial Reality: Most high-end panels today sit at 22–24% efficiency. To get even a 0.5% gain, manufacturers are spending billions.

- The Tandem Solution: By stacking a perovskite layer that “harvests” the blue light while the silicon “catches” the red/infrared light, we can push theoretical efficiency to 43%.

2. 2026 Milestone: From Lab Records to Field Deployment

The numbers are no longer just theoretical.

- New Records: In 2025, companies like LONGi and JinkoSolar shattered records, achieving certified tandem cell efficiencies as high as 34.85%.

- Commercial Shipping: Oxford PV (UK) has already begun shipping its first commercial-sized tandem modules with a 24.5%–26.9% efficiency, proving that perovskite can survive outside the lab.

3. The Economic “Game Changer”: Efficiency = Real Estate

Why does an extra 5% efficiency matter so much? It’s about LCOE (Levelized Cost of Energy) and space.

- Space-Constrained Markets: In countries like South Korea, Japan, or the UK, where land is expensive, a 30% efficient panel produces 25% more power from the same rooftop area.

- System Costs: High efficiency reduces the “Balance of System” (BOS) costs. You need fewer racks, less wiring, and less labor to generate the same Megawatt.

4. The Global Race: Who Will Scale First?

| Region | Strategy | Key Players |

| South Korea | “Super Gap” Technology & Mass Production | Hanwha Qcells, Jusung Engineering |

| Europe | IP Dominance & Early Commercialization | Oxford PV, Meyer Burger |

| China | Supply Chain Integration & Scale | LONGi, JinkoSolar, UtmoLight |

Hanwha Qcells is a particularly strong contender, aiming to start full-scale internal tandem cell mass production after June 2026. Their “Dream Solar” project aims to combine their world-class silicon base with high-durability perovskite layers.

5. The Remaining Hurdle: The “T80” Durability Test

The skeptics always point to durability. Silicon lasts 25 years; early perovskites lasted weeks.

However, as of 2026, research has pushed “T80” metrics (the time it takes to drop to 80% power) past the 1,000-hour mark in accelerated stress tests. We are now seeing the first 20-year warranties for tandem modules—a critical psychological bridge for bankability.

The Final Takeaway

The first era of solar was about making it cheap. The next era is about making it powerful. Tandem technology allows the industry to evolve without throwing away the trillions of dollars already invested in silicon infrastructure. It is an “upgrade,” not a “replacement.” As we move through 2026, the battleground has shifted: the companies that can scale high-efficiency tandem designs will own the next 20 years of the energy transition.

댓글 남기기