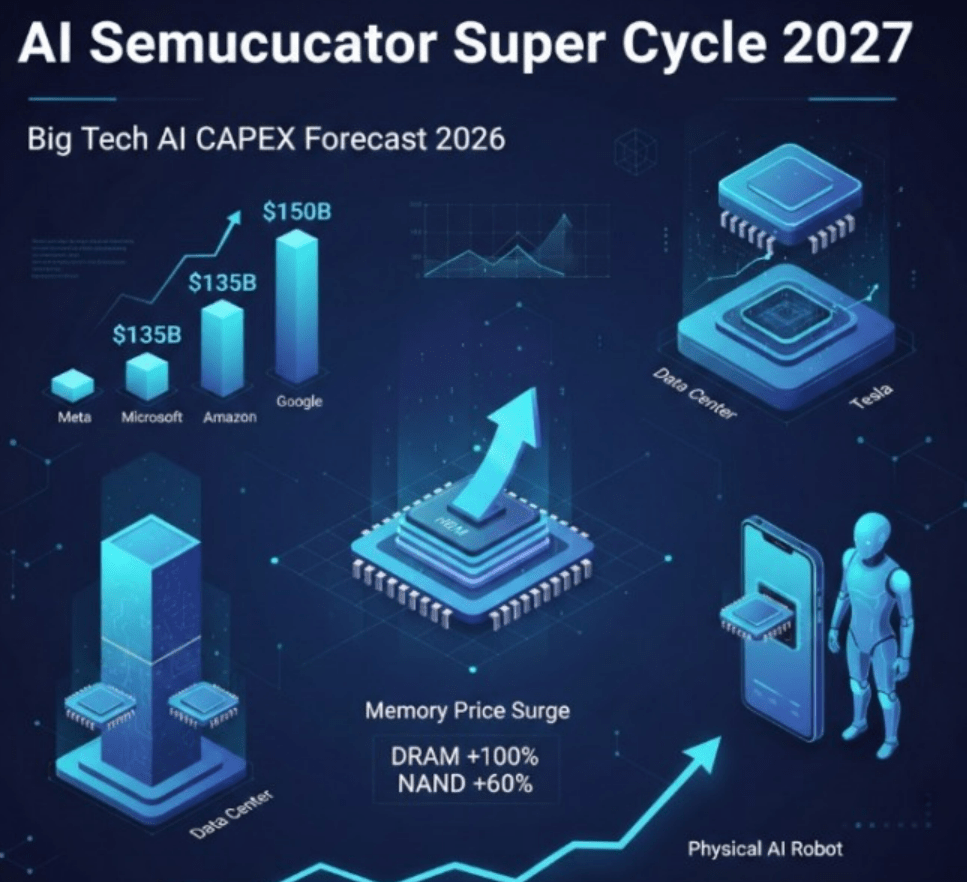

Every semiconductor cycle follows a rigid financial gravity. First, prices rise. Then, producers rerate. Finally, the “Big Spend” begins.

We’ve already seen the first two acts play out. Memory prices have stabilized, and producer stocks have been rewarded. Now, we are entering the third—and often most profitable—act: The migration of capital toward equipment, materials, and process components.

1. The Capital Flow Sequence

The pattern is predictable, yet many investors miss the hand-off.

- Rising prices fix the balance sheets of producers.

- Expanding CapEx translates into massive orders for equipment.

- Increased shipments lead to a surge in the consumption of raw materials.

While memory stocks have already priced in much of the recovery, the earnings for equipment and materials companies are only just beginning to show the impact. The “earnings expansion” is officially moving downstream.

2. Equipment: The First Port of Call

When a memory giant decides to spend, equipment suppliers are the first to get the call. This isn’t just about replacing old machines; it’s about a massive structural shift in how chips are made.

Key Drivers:

- The build-out of dedicated HBM production lines.

- Aggressive upgrades for high-layer NAND processes.

- New fab construction to meet 2026/27 demand.

Whether it’s global leaders like Applied Materials and Lam Research, or specialized players like Hanwha Precision (with TC bonders for HBM), these companies capture the first wave of capital as it leaves the producers’ pockets.

3. Materials: Growth That Runs on Autopilot

While equipment is about capacity, materials are about volume. As production ramps up, the revenue growth for materials companies becomes almost automatic.

- The Logic: More wafers = more chemicals, more gases, and more slurries.

- The Play: Companies like Hansol Chemical, Soulbrain, and Wonik Materials thrive here.

This segment is volume-sensitive, not price-sensitive. Once the production lines start humming, these companies enjoy highly visible, recurring revenue that scales directly with chip output.

4. Process Components: The “Advanced Node” Beta

As we push the limits of HBM and high-layer NAND, the “consumables” within the machines become more critical than ever. We are talking about high-temperature-resistant parts and ultra-durable precision modules.

As process complexity rises, these components shift from being “optional” to “essential.”

- Critical Players: Companies like TCK (SiC and quartz) and Wonik QnC.

- The Edge: Higher process difficulty leads to faster replacement cycles, meaning more frequent orders and stronger margins.

5. Why the Inflection Point is Now

We are currently seeing a rare alignment of three structural drivers:

- HBM expansion is happening years ahead of the demand curve.

- NAND is being revalued as the backbone of AI inference storage.

- CapEx budgets for 2026 are being revised upward across the board.

While memory producers often face price volatility and margin pressure late in the cycle, the equipment and materials sectors offer stronger visibility during this mid-to-late expansion phase.

Final Thought

Memory prices may start the fire, but equipment and materials keep it burning.

As capital expenditure resumes, the equipment sector catches the first wave of spending, materials scale with every chip shipped, and process components benefit from the sheer complexity of AI-grade silicon. If you want to see where the cycle is going, stop looking at the price of the chips and start looking at the tools and materials used to build them.

댓글 남기기