Why the 2026 Strategy is a Must-Watch for Long-Term Investors

LG Electronics is quietly but fundamentally reshaping its DNA. While many still view it through the lens of traditional home appliances, the company is aggressively pivoting toward robotics, energy solutions, and AI-driven infrastructure—the very sectors poised to define the next industrial cycle.

Here is a breakdown of how LG is positioning its portfolio for a structural shift by 2026.

1. 2026 Segment Outlook: High-Margin Evolution

- HS (Home Appliance & Air Solution): LG’s cash cow is evolving from a hardware seller to a service provider. By leveraging premium product mixes and subscription-based recurring revenue, LG is securing stable, predictable cash flow.

- VS (Vehicle component Solutions): This is no longer just about car displays. LG is integrating on-device AI and infotainment software, transforming itself from a component supplier into a system-level architect for Software-Defined Vehicles (SDV).

- ES (Energy Solutions): Perhaps the most underappreciated gem. AI data centers require massive cooling capacity. As power consumption explodes, LG’s high-efficiency chiller systems are positioning the company as a critical bottleneck-solver in AI infrastructure.

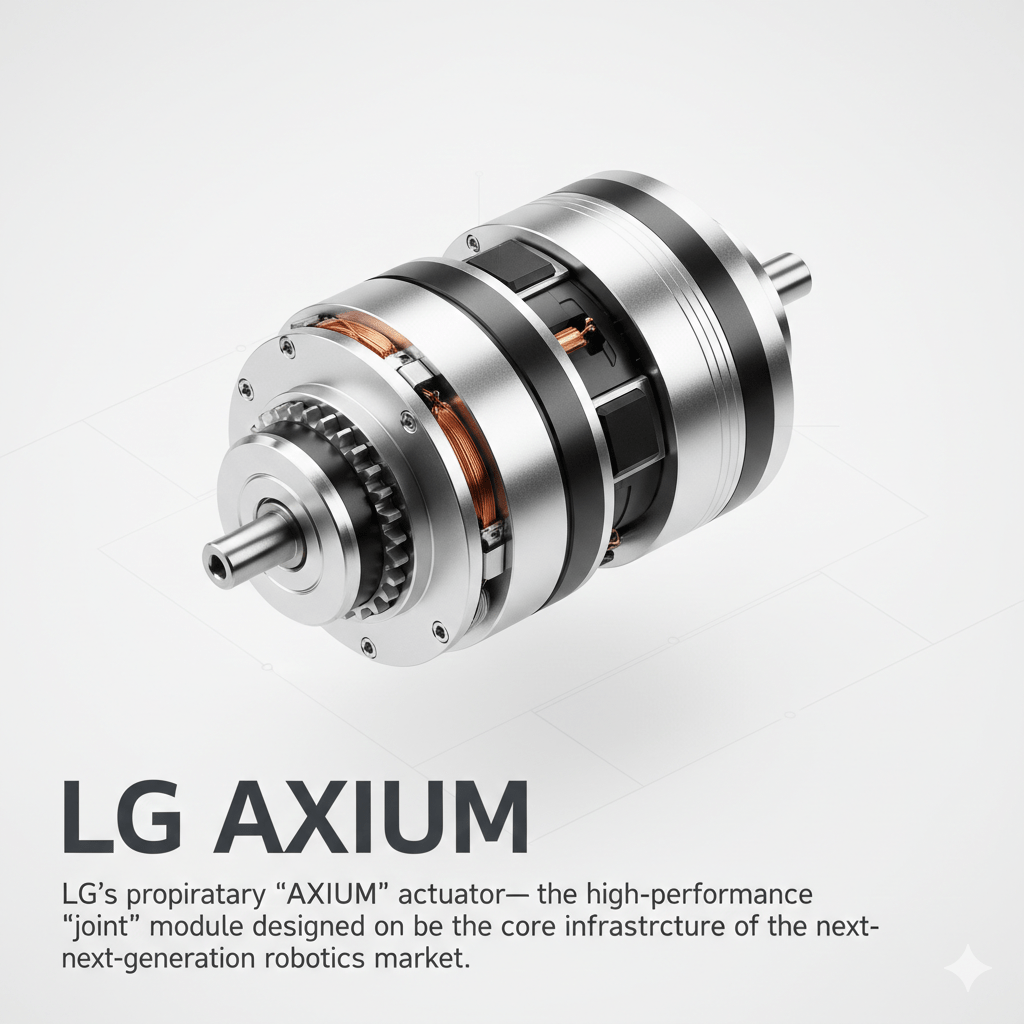

2. Robotics: Securing the “Skeleton” of the Industry

LG’s robotics play avoids a common tactical error: focusing only on the final product. Instead, they are securing the entire value chain.

- Home AI (“CLOi”): More than just a gadget, CLOi is designed as an AI agent integrated with the ThinQ ecosystem, driven by a platform-service model rather than a one-time hardware sale.

- Actuators (“AXIUM”): This is the hidden growth engine. By developing proprietary actuators—the “joints” of a robot—LG plans to begin external sales by 2027. Component businesses typically offer better scalability and higher strategic value than finished robots alone.

3. The Numbers: 2026 Consensus Trends 💰

The financial shift reflects this structural change. Market expectations for 2026 suggest a healthy upward trajectory:

| Metric | 2025 (Est.) | 2026 (Proj.) |

| Operating Profit | KRW 2.5T | KRW 3.1T |

| EPS | KRW 7,061 | KRW 9,287 |

| ROE | 6.0% | 7.6% |

Despite these improving fundamentals, LG’s valuation remains conservative (P/E ~11x), offering a potential margin of safety for patient investors.

Final Thoughts

LG Electronics is no longer just about TVs and refrigerators. For long-term investors, the real story isn’t about immediate robotics revenue; it’s about how LG is embedding itself into the infrastructure layer of the next tech cycle—from AI cooling to robotic joints.

댓글 남기기